Financing Restaurant Equipment for Your Kitchen

Financing restaurant equipment is all about getting the kitchen tools you need—the ovens, coolers, and prep tables—without having to pay a huge lump sum of cash upfront. It’s a smart strategy that lets you hold onto your capital for day-to-day operations while still outfitting your kitchen to run at its best.

Understanding Your Restaurant Equipment Financing Options

Let's be honest, outfitting a commercial kitchen is one of the biggest investments you'll make. But that massive capital outlay doesn't have to completely drain your bank account.

The world of equipment financing gives restaurant owners two main paths: you can either get a loan to buy the equipment outright, or you can set up a lease to essentially rent it for a set period. Each option has a different impact on your cash flow, your taxes, and whether you own the gear in the long run.

This isn't just some minor financial detail; it's a strategic decision that businesses everywhere are making. The equipment finance industry is huge, projected to grow from about USD 1.302 trillion to USD 1.437 trillion in just one year. That explosive growth shows just how vital these financing tools are for getting critical assets without crippling a budget.

The Two Core Paths: Loans and Leases

Think of it like getting a car. You can either buy it or lease it.

An equipment loan is the straightforward "buy" option. A lender gives you the money to purchase the equipment, and you own it from the moment it lands in your kitchen. You’ll make regular payments over a set term until the loan is paid off, building equity in an asset that shows up on your business's balance sheet. This is a great route for those durable, long-lasting workhorses like commercial ovens or walk-in coolers.

An equipment lease, on the other hand, is more like a long-term rental. You pay a monthly fee to use the equipment for a specific period. When the lease term is up, you usually have a few choices:

- Send the equipment back and upgrade to a newer model.

- Buy the equipment for whatever its fair market value is at that time.

- Extend the lease for another term.

Leasing is especially appealing for technology that can become outdated quickly, like POS systems, or for new restaurants trying to keep their initial costs as low as possible. You can dive deeper into the specific benefits of restaurant equipment financing in our detailed guide.

To make things a bit clearer, let's break down the key differences between these two financing routes.

Equipment Loan vs. Equipment Lease at a Glance

| Feature | Equipment Loan | Equipment Lease |

|---|---|---|

| Ownership | You own the equipment from day one. | You don't own it. The leasing company does. |

| Upfront Cost | Usually requires a down payment (10-20%). | Often little to no down payment required. |

| Monthly Payments | Typically higher, as you're paying off the full cost. | Generally lower, as you're only paying for depreciation. |

| End of Term | Once paid off, you own the asset free and clear. | You can return, purchase, or renew the lease. |

| Flexibility | Less flexible; you're committed to the equipment. | More flexible; easy to upgrade to newer technology. |

| Balance Sheet | The equipment is listed as an asset. | The equipment is not on your balance sheet. |

Ultimately, picking the right option depends on your business goals and financial situation. Both paths are designed to get you the equipment you need without a massive cash hit.

The choice between a loan and a lease really boils down to your long-term goals. Do you want to build assets and own your equipment for its entire lifespan, or do you prioritize lower monthly payments and the flexibility to upgrade? Answering that question is the first real step toward making a sound financial decision for your restaurant.

Auditing Your Kitchen Needs and Budget

Before you even think about talking to a lender, the most important thing you can do is get your numbers buttoned up. Getting financing for restaurant equipment isn't just about asking for a check; it's about showing up with a realistic, well-researched plan that proves you know exactly how you'll put every dollar to work. That process starts with an honest look at your kitchen and a seriously detailed budget.

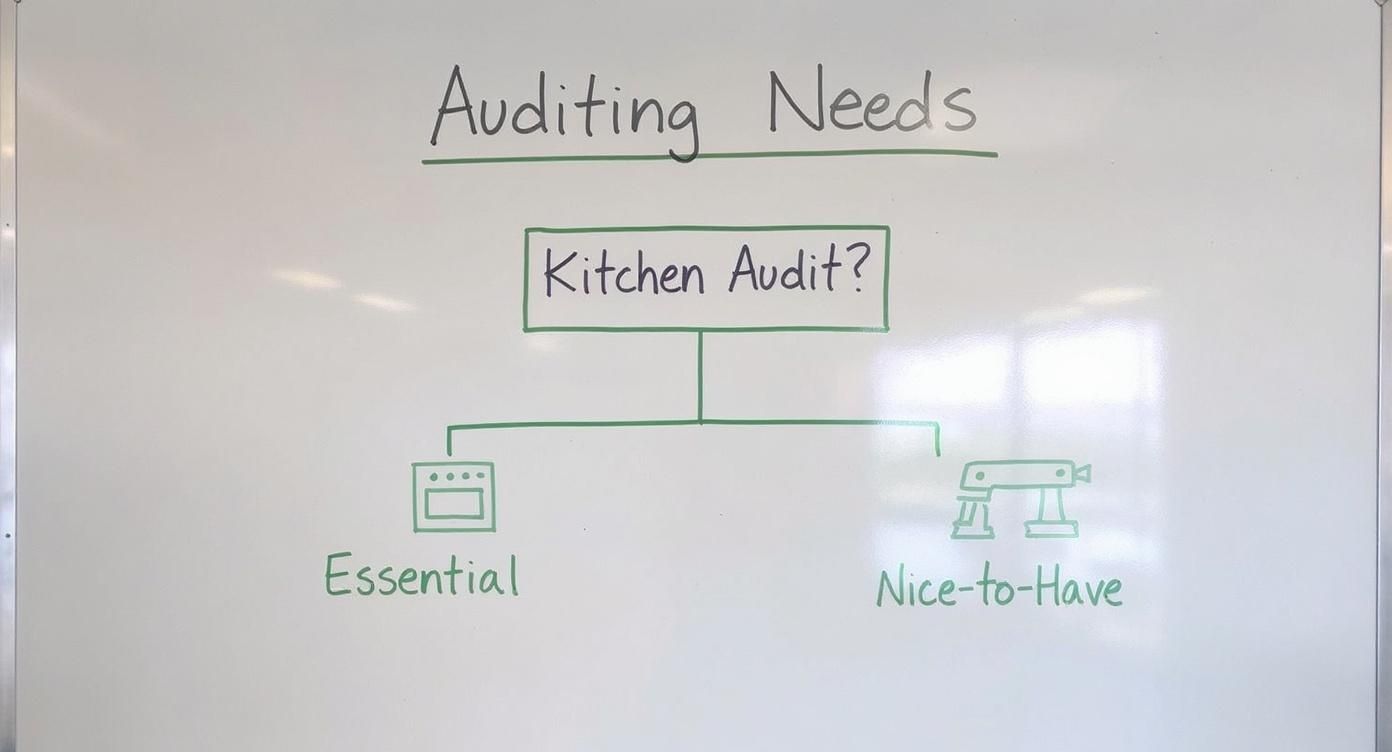

Walk through your kitchen and start making a list of everything you might need. The trick is to separate the absolute must-haves from the nice-to-have upgrades. If you're opening a pizzeria, a big, reliable deck oven is a non-negotiable workhorse. That fancy automated dough sheeter, on the other hand? That’s a "desirable" that can probably wait. Lenders want to see this distinction because it shows you're focused on the core assets that will actually generate revenue.

Identifying Essential vs. Desirable Equipment

Making two separate lists is a simple trick, but it forces you to clarify what you truly need to finance right now.

- Essentials: These are the items that are absolutely critical for your menu and day-to-day operations. We're talking about your commercial ranges, refrigeration units, and the indispensable three-compartment sink. Your restaurant simply can't open its doors without them.

- Desirables: This list is for equipment that would be great to have—maybe it would boost efficiency or let you add a new menu item—but it isn't vital on day one. Think of a vacuum sealer for that sous vide dish you've been dreaming of, or a high-end espresso machine in a diner that primarily serves lunch.

This exercise isn't just for you; it demonstrates financial discipline and helps you build a budget that puts first things first.

Building a Realistic Budget Beyond the Sticker Price

Once you’ve nailed down your essentials, it’s time to get real quotes. Don't just pull the first price you see online. Reach out to several suppliers for both new and used options to get a feel for the real market rate.

Here's where a lot of operators make a mistake: they only budget for the sticker price of the equipment. A lender wants to see that you've thought through all the associated costs, which can easily add another 15-25% to your total. Your budget needs to include line items for things like shipping, professional installation, any potential plumbing or electrical work, and initial maintenance.

For a clearer picture of your total financial commitment, you can use our guide to calculate your costs before cooking with a restaurant equipment finance calculator.

A detailed budget is your most powerful negotiation tool. It’s not just a list of costs; it's a narrative that tells a lender you've done your homework, understand the total financial picture, and have a concrete plan for every dollar you're requesting.

When you present a budget that accounts for these "hidden" costs, you instantly shift from being just another hopeful applicant to a serious business partner in the eyes of any financing provider. It proves you’re not just planning for a purchase—you're planning for success.

Choosing Between an Equipment Loan and a Lease

Figuring out how to finance your restaurant equipment isn't about finding the single "best" option. It's about finding the one that fits your business strategy like a glove. The choice between buying with a loan or leasing comes down to how you think about ownership, cash flow, and the lifespan of the equipment itself. This is a strategic call that goes way beyond just looking at the monthly payment.

For instance, if you're building a pizzeria around your signature brick ovens, an equipment loan is probably the way to go. Those ovens are the heart of your brand—they're durable, long-lasting assets. Owning them builds equity on your balance sheet, and once that loan is paid off, they become a valuable, cost-free part of your operation for years to come.

When an Equipment Loan Makes the Most Sense

An equipment loan is your best bet when you're investing in the core, foundational pieces of your kitchen—the stuff that won't be obsolete in a couple of years.

- Long-Lifespan Equipment: We're talking about the heavy-duty workhorses like commercial ranges, walk-in coolers, and high-quality stainless steel prep tables.

- Building Business Equity: If your goal is to grow the value of your business, owning your assets is huge. Lenders see owned equipment as collateral, which can make it easier to get more financing down the road.

- Predictable, Fixed Costs: With a loan, your payments are fixed. That makes it incredibly simple to budget for the long haul without worrying about surprise cost increases.

When Leasing Is the Smarter Play

On the other side of the coin, leasing offers a ton of flexibility that's perfect for certain types of gear and business situations. It’s a fantastic strategy for preserving cash, which is especially critical for new restaurants just getting off the ground.

Picture a trendy cafe that wants to offer the latest and greatest in espresso technology. Leasing a high-end espresso machine lets them stay on the cutting edge without a massive upfront cash drain. In two or three years, when a newer, more efficient model hits the market, they can simply upgrade when their lease term is up. Our guide on how to lease restaurant equipment without losing your lunch money dives deeper into these strategies.

This decision tree helps visualize that initial thought process, guiding you to separate the essential workhorses from items that might be better suited for a lease.

As the infographic shows, the first step is always to audit what you truly need, making a clear distinction between core operational necessities and desirable upgrades that could be leased.

Let's break down the financial nuances even further. This table gets into the nitty-gritty of how each option impacts your books and operations.

Deep Dive Comparison Loan vs Lease Financial Implications

| Consideration | Equipment Loan Details | Equipment Lease Details |

|---|---|---|

| Ownership | You own the equipment outright once the loan is fully paid. It becomes a business asset. | You never own the equipment. You're essentially renting it for a set period. |

| Upfront Cost | Requires a down payment, typically 10-20% of the total equipment cost. | Usually requires only the first and last month's payment upfront, preserving cash flow. |

| Monthly Payments | Generally higher than lease payments because you're paying off the principal and interest. | Lower monthly payments since you are only covering the equipment's depreciation, not its full value. |

| Total Cost | The total cost over the loan term is often lower than the total cost of leasing for the same period. | The total cost over the lease term can be higher because you're paying for convenience and flexibility. |

| Asset Depreciation | You can claim tax deductions for depreciation, which can be a significant tax benefit. | You cannot claim depreciation. The leasing company owns the asset and gets this benefit. |

| Tax Deductions | Only the interest portion of your loan payment is tax-deductible. | The entire lease payment is typically considered an operating expense and is fully tax-deductible. |

| End of Term | Once paid off, you have a valuable asset with no more payments. | You must return the equipment, renew the lease (often at a new rate), or buy it at fair market value. |

| Flexibility | Less flexible. You're committed to the equipment for its entire useful life. | Very flexible. Easy to upgrade to newer technology at the end of the lease term. |

Ultimately, weighing these factors will help you see which path aligns better with your restaurant's financial health and long-term goals.

Unpacking the Tax Implications

The way taxes are handled for loans and leases is another critical piece of the puzzle. With an equipment loan, you own the asset from day one. This means you can deduct the interest you pay on the loan each year. You also get to claim depreciation on the equipment, which can lead to some serious tax savings, especially in the first few years of ownership.

Lease payments, however, are usually treated differently. Since you don't own the equipment, the entire monthly lease payment is often considered an operational expense. This allows you to deduct the full payment from your taxable income, which can simplify your accounting and lower your overall tax bill.

The choice ultimately hinges on a simple question: Is this piece of equipment a long-term asset that builds value, or is it a tool that needs to stay current? Answering this will guide you to the right financing structure for your restaurant.

The demand for modern kitchen tools is driving huge growth in the restaurant equipment market. Valued at around USD 4.8 billion, it's expected to rocket to USD 10.2 billion within a decade. This boom underscores the industry's continuous need for efficient, technologically advanced gear, making these financing decisions more important than ever.

Preparing an Application That Gets Approved

Think of your financing application as more than just a request for money. It’s your chance to tell a compelling story about your restaurant's stability, its potential, and why this new equipment is a smart investment—not just for you, but for the lender, too.

Underwriters see a mountain of applications every day. Yours needs to rise to the top by being clear, thorough, and professional. Showing up with meticulously organized paperwork immediately signals that you're a serious operator who runs a tight ship, both in the kitchen and on the balance sheet. It’s a simple step that dramatically boosts your chances of getting that "yes."

Gathering Your Essential Financial Documents

Before you even think about filling out a form, get your financial documents in order. Lenders almost always ask for the same core paperwork, so having everything ready to go will make the entire process faster and smoother.

Your application package needs a solid foundation of clean, accurate financial statements. This typically includes:

- Profit and Loss (P&L) Statements: You'll want the last two or three years to showcase your revenue, costs, and, most importantly, your profitability.

- Balance Sheets: These provide a snapshot of your assets, liabilities, and owner's equity at a specific point in time.

- Cash Flow Statements: This is crucial. It details how cash moves through your business and proves you have the liquidity to handle monthly payments.

- Business and Personal Tax Returns: Lenders will usually ask for the last two years to verify your income and get a complete financial picture.

The clarity of these documents can make or break your application. If you’re not a numbers expert, that’s okay. There are some great resources for accurately preparing financial reports that can help you get your paperwork lender-ready.

Crafting a Compelling Business Plan and Proposal

Numbers tell part of the story, but your application also needs a narrative. This is where your business plan comes in. No, you don’t need to hand over a 50-page document. A concise summary that speaks directly to the financing request is far more effective.

Zoom in on the sections an underwriter cares about most. Your financial projections should clearly show how the new equipment will impact your bottom line. Will that new high-efficiency convection oven let you boost your catering output by 25%? Will a modern POS system slash order errors and improve table turnover? Use specific, believable numbers.

Your market analysis should briefly touch on your customer base and competitors, proving you have a firm grasp of your place in the local market. It’s about demonstrating you have a solid strategy, not just a wish list.

The best equipment proposals connect the dots for the lender. Don't just say you need a new fryer. Explain that a specific model will cut your oil costs by $300 a month and increase your fried chicken output by 40% during peak hours, directly boosting revenue.

Telling the Story Behind the Numbers

Finally, don’t be afraid to add a little context. A brief cover letter or executive summary can be the perfect place to explain any blips in your financial history. Maybe a slow season was due to major road construction out front, or a dip in profits was the result of a planned renovation.

Being upfront builds trust. It shows you know your business inside and out and aren't trying to hide anything. When you combine pristine financial documents with a clear, strategic story, your application for financing restaurant equipment will stand out for all the right reasons.

What Happens After You Hit ‘Submit’? Navigating the Approval Timeline

So you’ve submitted your financing application. That’s a huge step, but the real work on the lender’s side is just getting started. This next phase is called underwriting, and it’s where a real person scrutinizes your request to figure out the risk and decide if your business is a solid bet. It’s not some mysterious process; they’re looking at a pretty standard set of numbers to get a clear picture of your restaurant's health.

Their review really boils down to a few key things. Your business credit score and how long you’ve been in operation give them a quick snapshot of your stability. But what they really dig into are your current cash flow statements. At the end of the day, that’s what shows your real-world ability to take on a new monthly payment.

What to Expect During the Review

Once you’re in the queue, the timeline can vary quite a bit. A straightforward equipment lease might get a green light in as little as 24 to 48 hours, especially if your credit is strong and your financials are clean. More complicated equipment loans, particularly for bigger-ticket items, could take anywhere from a few days to a couple of weeks as the underwriter does a much deeper dive.

Don’t panic if the lender comes back asking for more documents. This is a completely normal part of the process and definitely not a sign that you’re headed for a denial. They might ask for things like:

- An updated bank statement to confirm your recent cash flow.

- The specific invoice from your equipment supplier.

- A bit of clarification on a particular expense on your P&L statement.

The best thing you can do to keep things moving is to respond to these requests quickly and accurately. Delays here are almost always caused by slow responses.

A request for more documents isn't a red flag—it's an opportunity. It shows the lender is seriously considering your application and just needs to fill in a few gaps. View it as a chance to reinforce the strength of your business.

Remember, the demand for modern kitchen tools is massive. The global restaurant equipment market, valued at around USD 92.89 billion, is expected to skyrocket to USD 206.07 billion within a decade. This incredible growth shows just how much capital is being invested in restaurants worldwide. Lenders want to be a part of that, and they are actively looking to fund solid, well-prepared operators. You can dig into these restaurant equipment market trends to learn more.

Decoding Your Financing Offer

When that approval email finally lands in your inbox, it will come with a financing offer. This document is dense with important details, and you absolutely need to understand them before you sign anything. It’s tempting to just look at the monthly payment, but the real story is in the fine print.

Pay close attention to the interest rate or factor rate, since this is what determines the total cost of the money you’re borrowing. You’ll also want to hunt down and identify every single associated fee, like origination or documentation fees, which can add to the overall expense. Finally, double-check the repayment schedule and term length to make sure it aligns with your restaurant’s cash flow projections.

Knowing how to read this offer gives you the power to ask smart questions, negotiate for better terms, and confidently pick the financing that will actually help your business thrive in the long run.

Common Questions About Financing Restaurant Equipment

When you're looking into financing restaurant equipment, a lot of practical questions pop up. Getting straight answers is the only way to move forward with confidence. Let's tackle some of the most common things we hear from restaurant owners, so you have the info you need.

A big one is always about credit scores. While there isn't one magic number, having a personal credit score of 650 or higher is a great starting point. It usually opens the door to more options and better rates.

But don't panic if your score isn't perfect. Some lenders specialize in working with business owners who have less-than-ideal credit, so financing is definitely not off the table. They’ll also look at other factors, like how long you've been in business and your monthly revenue.

Can You Finance Used Equipment?

Absolutely. Financing used restaurant equipment is a common—and very smart—way to lower your upfront investment. Lenders are generally happy to finance pre-owned gear, especially for durable workhorses like ovens, mixers, and refrigerators that hold their value well.

The process is pretty much the same as financing new equipment. A lender will want to see an invoice or bill of sale from a reputable dealer. They'll also assess the equipment's value and how much life it has left to figure out the loan or lease terms. Just know that the repayment term for used gear might be a bit shorter than for something brand-new.

A quick tip from my experience: When you're financing used equipment, make sure you're buying from a trusted source. A lender feels much more comfortable when they can see clear documentation on the item's condition and maintenance history.

What About Soft Costs Like Installation?

This is a fantastic question, because those "soft costs" can really add up. The good news is that many financing agreements can be structured to cover more than just the sticker price of the machine itself.

It's often possible to bundle these related expenses right into your financing package:

- Installation Fees: This covers the cost of having a professional set up complex machinery, like a walk-in cooler or a commercial hood system.

- Shipping and Delivery Charges: You can roll the freight costs into the total amount financed so you don't have to pay for it out of your working capital.

- Training Costs: For some highly specialized equipment, the cost to get your staff trained up can sometimes be included, too.

Always ask a potential lender about this upfront. A good financing partner gets it—the equipment is useless without proper installation. They'll often work with you to build a package that covers the entire project, not just the hardware. This approach really simplifies your books and keeps your cash free for day-to-day operations.

At The Restaurant Warehouse, we provide flexible and straightforward financing solutions built for the realities of the restaurant world. We're here to help you get the essential equipment you need with payment plans that protect your cash flow. Explore your options and get your kitchen ready for success by visiting The Restaurant Warehouse.

About The Author

Sean Kearney

Sean Kearney is the Founder of The Restaurant Warehouse, with 15 years of experience in the restaurant equipment industry and more than 30 years in ecommerce, beginning with Amazon.com. As an equipment distributor and supplier, Sean helps restaurant owners make confident purchasing decisions through clear pricing, practical guidance, and a more transparent online buying experience.

Connect with Sean on LinkedIn, Instagram, YouTube, or Facebook.