Kitchen Equipment Leasing: What to Know Before You Sign

Bringing your restaurant vision to life is thrilling, but outfitting the kitchen can drain your startup capital before you even open. This is where kitchen equipment leasing offers a smarter path forward. Instead of buying everything outright, you get access to high-quality ovens, freezers, and other essential appliances for a fixed monthly fee. It’s a way to build a top-tier, fully-equipped kitchen right now, while keeping your cash free for other crucial needs like marketing, inventory, and hiring your team.

How Does Kitchen Equipment Leasing Work?

So, what does leasing really mean in practice? Imagine you're building a professional kitchen. Instead of buying an empty building and then spending a fortune filling it yourself, leasing is like moving into a space that’s already equipped with everything you need. It’s a financial tool that empowers restaurant owners to get the necessary tools of the trade without emptying their bank accounts before the doors even open.

It’s a pretty straightforward partnership:

- You (the lessee) are the restaurant or food business owner who needs the equipment.

- A finance company (the lessor) steps in to purchase the equipment for you.

- The supplier (like us at The Restaurant Warehouse) is where you pick out all the gear you want.

Essentially, you choose the exact equipment you need, the leasing company buys it for you, and you make regular monthly payments to them for a set period. Simple as that.

How Leasing Plays Out in Practice

Let's make this real. Say you're opening a new café and have your eye on a state-of-the-art $15,000 espresso machine. Instead of writing that huge check, you opt for a lease. The leasing company buys the machine, and you pay them a much more manageable monthly fee, maybe around $400 for 36 months. This move keeps your cash reserves healthy, giving you the funds you need for a killer grand opening and hiring your first team of talented baristas.

This model has become a go-to for modern foodservice businesses. With the explosion of food trucks, pop-up concepts, and cloud kitchens, there's a huge demand for flexible, cost-effective ways to get equipped. You can find more data on these evolving foodservice trends and their impact on equipment acquisition.

A lease agreement is a strategic bridge between needing state-of-the-art kitchen tools and maintaining financial stability. It empowers you to build a competitive kitchen without the burden of immediate, large-scale ownership costs.

The Application and Approval Process

When you're ready to lease your kitchen equipment, you'll find the application process is refreshingly simple. It's designed to be fast so you can get back to business. First, you'll browse and select the gear you need—from refrigerators to deep fryers. Once you have your list, you can apply for financing. Many applicants get approved in under a minute through straightforward restaurant equipment financing options. This quick turnaround means you can secure the tools you need to get your kitchen operational without long, stressful waits.

One of the biggest advantages of equipment leasing is its flexibility with credit. You don't need a perfect credit score to qualify. Many online lenders work with new businesses or entrepreneurs who are still building their credit history. This accessibility is a game-changer, especially for first-time restaurant owners who might not have years of business credit to back them up. It opens the door for more people to pursue their culinary dreams without being held back by traditional lending barriers.

To complete the application, you'll need to provide some basic details. This usually includes your Social Security number, the name and email of the business owner, your annual business income, and either bank account or credit/debit card information. Having this information ready will make the process even smoother. The leasing company uses these details to quickly assess your application and determine your financing options, keeping the paperwork to a minimum so you can focus on your menu, not on forms.

Worried about how applying might affect your credit? You can put that concern aside. Most leasing companies let you check your rate without any impact on your credit score. You’ll often receive an instant decision, so you’ll know exactly where you stand right away. This allows you to explore your leasing options confidently, without any negative marks on your financial record. The entire system is built for speed and convenience, helping you make informed decisions quickly and get your restaurant up and running.

How Does Leasing Stack Up?

Understanding all your options is the first step toward making a smart financial move for your business. While leasing is a powerful tool, it’s important to see how it stacks up against renting and buying outright. Each method is designed for a different business need and financial strategy.

For a deeper dive, check out our comprehensive guide to leasing restaurant equipment.

Here’s a quick breakdown to help you see the key differences at a glance.

Breaking Down Leasing vs. Renting vs. Buying

| Attribute | Leasing | Renting | Buying |

|---|---|---|---|

| Ownership | Option to own at lease end | No ownership | Immediate ownership |

| Cost Structure | Fixed monthly payments | Short-term, often higher rate | Full upfront cost |

| Flexibility | Long-term (1-5 years) | Short-term (daily/weekly) | Permanent commitment |

| Maintenance | Typically lessee's responsibility | Often included in rental fee | Owner's responsibility |

Ultimately, the right choice depends on your business's financial health, long-term goals, and how much flexibility you need.

Why Leasing Your Kitchen Equipment is a Smart Money Move

Deciding how to outfit your kitchen isn't just about operations—it’s a massive financial decision. While buying equipment outright might feel like a straightforward investment, leasing offers a powerful set of financial advantages that can seriously strengthen your restaurant's bottom line and give you the stability to thrive. It’s a strategic move for building a more resilient, agile business.

Let’s imagine Maria, a passionate entrepreneur opening her first café. She’s got a solid business plan and a crystal-clear vision, but her startup capital is limited. The high-end espresso machine, convection oven, and commercial refrigeration she needs add up to $50,000—a sum that would eat up most of her funds right out of the gate.

By choosing to lease, Maria completely sidesteps that huge initial expense. Instead of draining her bank account, she gets all the equipment she needs for a manageable monthly payment. This one decision fundamentally changes her financial outlook, preserving a vital cash cushion for payroll, marketing, and all the unexpected challenges that pop up.

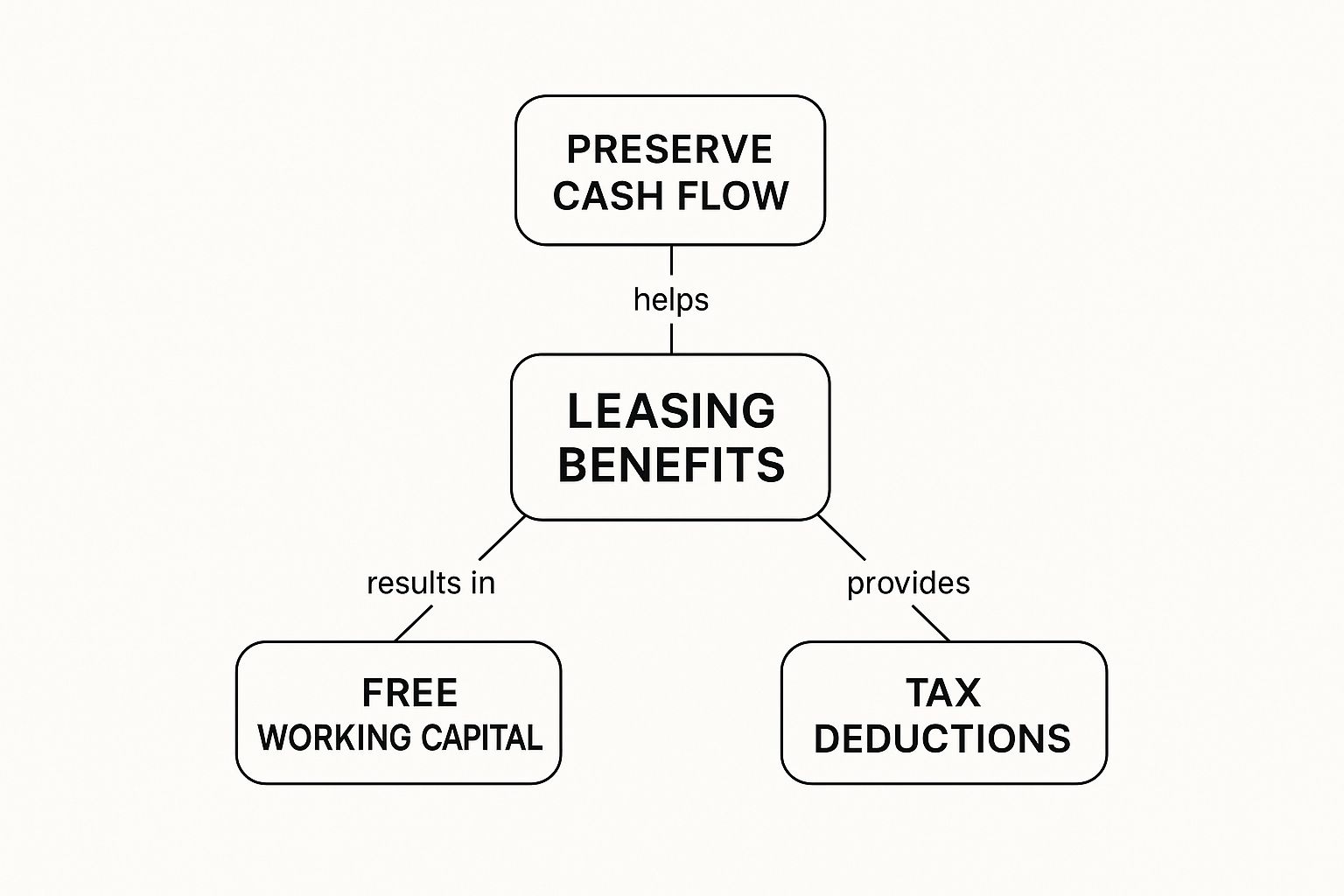

This infographic breaks down the primary financial perks of going with a lease.

As you can see, the benefits are all connected. Preserving cash flow is the central pillar that supports greater financial flexibility and some nice potential tax advantages.

Keep Your Cash Flow Healthy

Cash flow is the absolute lifeblood of any restaurant. Leasing acts as a powerful protector of this critical resource. By turning a massive, one-time capital expense into smaller, predictable operational payments, you keep more money in the bank for your day-to-day needs. It’s an approach that’s quickly becoming standard for smart operators.

In fact, the equipment leasing sector in North America is on track for significant growth by 2030, mostly because it helps small and mid-sized businesses slash upfront costs and keep their tech current. You can find more data on why so many foodservice operators are shifting to leasing models.

This preserved cash gives you the breathing room to handle the unpredictable nature of the restaurant world—from a slow season to a sudden repair—without risking financial distress.

Put Your Working Capital Toward Growth

Beyond just staying afloat, that preserved cash becomes your working capital—the fuel for your business's growth. With funds not tied up in equipment that’s losing value, you can invest in areas that generate immediate returns.

For Maria, this meant she could:

- Launch a targeted digital marketing campaign to create buzz before her grand opening.

- Hire an experienced head barista to guarantee top-quality coffee from day one.

- Buy a larger initial inventory of premium beans and local pastries.

These investments, all made possible by leasing, directly help attract customers and build a strong brand, setting her up for long-term success.

Budget Better with Predictable Payments and Tax Breaks

Leasing also makes your financial planning a whole lot simpler. Lease payments are usually fixed, which means you know exactly how much to budget for your equipment every month, quarter, and year. This predictability gets rid of surprises and makes your financial forecasts far more accurate.

By transforming a volatile capital expense into a stable operational cost, leasing gives you greater control over your budget and financial future.

On top of that, leasing can offer some significant tax benefits. In many cases, those monthly lease payments can be deducted as an operational business expense, which can lower your overall taxable income. It’s a financial win-win.

Of course, the specifics will depend on your lease structure and your business. It’s always smart to chat with a tax professional to understand the full picture. To learn more about how different financing structures impact your business, check out our guide on the benefits of restaurant equipment financing. By understanding these advantages, you can make a truly informed decision for your kitchen's future.

Protect Your Credit Lines

Here’s another financial perk you might not have considered: leasing helps protect your existing lines of credit. Because a lease isn't typically recorded as a major debt on your financial statements, it leaves your other credit sources—like business loans or credit cards—completely untouched. This is a huge advantage. It means you have your full borrowing power available for other critical needs, whether it's covering a payroll gap during a slow month or seizing a sudden opportunity to expand your patio. Instead of tying up your credit on depreciating assets like a deep fryer, you keep your financial safety net intact for true emergencies or growth investments.

Lock in Fixed Payments Against Inflation

In a world where prices seem to be constantly on the rise, leasing offers a welcome dose of stability. Your lease payments are typically fixed for the entire term. This means that while the cost of new refrigerators or prep tables might increase due to inflation, your monthly payment won't budge. This predictability is a powerful tool for budgeting and can lead to significant savings over the life of the lease. By converting a large, unpredictable purchase into a series of fixed operational costs, you shield your business from economic volatility. You can find more details on how these payment structures work by exploring different restaurant equipment financing options, but the bottom line is simple: you gain control and peace of mind.

The Downsides: Potential Risks of Leasing

Leasing sounds pretty great, right? And for many businesses, it absolutely is. But just like any major financial decision, it’s not a one-size-fits-all solution. It’s important to walk into a lease agreement with your eyes wide open, fully aware of the potential trade-offs. While the immediate benefits like preserving cash are compelling, there are some long-term factors that could impact your finances and operational freedom down the road. Thinking through these potential risks isn't about scaring you away from leasing; it's about empowering you to make the most strategic choice for your restaurant's unique situation. For some, these downsides might be minor compared to the benefits, while for others, they might signal that another path, like financing a purchase to own your equipment, is a better fit.

Let's be real: the fine print matters. A lease is a binding contract, and understanding its terms is crucial to avoiding future headaches. From total cost over time to what happens if your business needs to pivot, these are the details that separate a smart financial move from a costly mistake. By looking at the complete picture—both the shiny upsides and the potential downsides—you can confidently weigh your options. This balanced perspective ensures you're not just solving an immediate cash flow problem, but also setting your business up for sustainable, long-term success. Let's break down some of the key considerations you'll want to have on your radar.

Higher Long-Term Costs

The biggest draw of leasing is the low upfront cost, but it's essential to calculate the total expense over the entire lease term. When you add up all the monthly payments, you'll often find that you've paid significantly more than the equipment's actual retail price. This is because the lease payments include interest and fees from the financing company. If your credit isn't perfect, those interest rates can be quite high, further inflating the total cost. Before signing, always do the math to understand the full financial commitment. The Small Business Administration offers great resources for comparing the true cost of leasing versus buying.

No Equity or Ownership

When you lease equipment, you're essentially renting it for a long period. At the end of the term, you have nothing to show for all those payments—no asset, no equity. Unlike equipment you own, you can't sell a leased deep fryer or use a leased refrigerator as collateral to secure another business loan. This lack of ownership can limit your financial flexibility. Owning your equipment means it's a tangible asset on your balance sheet, contributing to your business's net worth. With a lease, the equipment always belongs to the leasing company, so it never helps build your business's value.

Long-Term Commitment and Cancellation Fees

A lease is a contract, and most are designed to be ironclad for a set period, often several years. This can be a problem if your business needs change. What if that specialty oven you leased is no longer needed because you've revamped your menu? Or what if a newer, more efficient model comes out? You're typically locked into your payments for the full term, regardless of whether you're still using the equipment. Getting out of a lease early is rarely easy or cheap; you'll likely face substantial cancellation fees that can negate any initial savings. This rigidity is a key factor to consider, especially for new or rapidly evolving restaurant concepts.

Strict Rules on Use and Maintenance

Don't forget to read the fine print on upkeep. Most lease agreements come with specific rules about how you can use the equipment and who is responsible for maintenance and repairs—which is almost always you. You might be required to follow a strict maintenance schedule or use specific service providers. If the equipment breaks down due to what the lessor considers misuse or neglect, you could be on the hook for expensive repairs or penalty fees. These clauses are designed to protect the leasing company's asset, but they can limit your operational freedom and add unexpected costs if you're not careful.

Choosing the Right Type of Equipment Lease

When you start looking into commercial kitchen equipment leasing, you’ll quickly find that not all leases are the same. The agreement you sign will almost always fall into one of two categories, and each one has a completely different financial impact on your business. Nailing this distinction is the key to picking a path that actually matches your long-term goals.

Think of it like getting a car. Do you want to rent it for a few years and then easily swap it for a newer model? Or do you plan to drive it until the wheels fall off and eventually own it? Those two mindsets perfectly capture the difference between the two main types of equipment leases.

The two structures you'll run into are Capital Leases and Operating Leases. Knowing which one fits your restaurant's financial strategy is one of the most important decisions you'll make.

Capital Leases: The Path to Ownership

A Capital Lease, often called a finance lease, is basically your "rent-to-own" option. It’s built for business owners who fully intend to keep the equipment for its entire useful life. This is the route you take for the foundational workhorses of your kitchen—the heavy-duty stuff you can't imagine operating without.

Imagine you're opening a steakhouse and need a custom-built, walk-in freezer. That isn't something you’ll want to trade in a few years; it’s a long-term investment that’s central to your whole operation. A capital lease lets you finance this major purchase over time, with the clear expectation that you will own it when the lease is up.

Under this structure, the lease often includes a buyout option at the end, which can be as low as $1. Because ownership is the goal, the equipment is treated like an asset on your balance sheet, and you can often depreciate it for tax purposes, just like you would with an outright purchase.

Operating Leases: The Flexible Rental Option

On the flip side, an Operating Lease is much more like a long-term rental agreement. This is the perfect choice for equipment you might want to upgrade frequently or that has a shorter technological lifespan. Think about point-of-sale (POS) systems or specialty cooking gadgets where newer, more efficient models come out every couple of years.

For example, a trendy pop-up that changes its menu concept with the seasons might use an operating lease for a high-tech combi oven. This gives them access to the latest cooking technology without the long-term commitment. When the lease ends in two or three years, they can simply return the oven and lease the newest model.

An operating lease is a strategic tool for staying flexible. It allows your kitchen to stay current with technology and adapt to changing business needs without being weighed down by aging assets.

With an operating lease, the monthly payments are treated as a straightforward operational expense on your income statement. The equipment itself doesn't show up as an asset or liability on your balance sheet, which is a big plus for businesses that want to keep their financial statements lean.

Capital vs. Operating Lease: A Quick Comparison

Choosing the right type of commercial kitchen equipment leasing really comes down to your game plan. Do you want to own the asset for the long haul, or do you value the freedom to upgrade and adapt? Your answer will point you straight to the lease that serves your business best.

This simple table breaks down the key differences to help you see it all at a glance.

| Feature | Capital Lease (Finance Lease) | Operating Lease |

|---|---|---|

| Primary Goal | Ownership at the end of the lease | Use of the equipment for a set period |

| Balance Sheet | Appears as both an asset and a liability | Does not appear on the balance sheet |

| End of Term | Typically a purchase for a pre-set price (e.g., $1 Buyout) | Return, renew, or purchase at Fair Market Value (FMV) |

| Best For | Core, long-lifespan equipment like walk-in coolers or ovens | Tech-heavy or short-lifespan items like POS systems |

Ultimately, both lease types are powerful tools. The key is knowing which one to use for the job at hand to keep your kitchen running smoothly and your finances in great shape.

How to Secure an Equipment Lease Step-by-Step

Diving into the world of commercial kitchen equipment leasing can feel like a lot to take on, but it gets a whole lot simpler when you break it down. Think of it like following a new recipe—each step builds on the last, and if you follow the process, you’ll end up with something great. This five-step roadmap will take you from the initial planning stage all the way to signing on the dotted line with total confidence.

Following these steps won't just make the process smoother; it will put you in the best position to lock in great terms for your business. Ready to get started?

Step 1: What Equipment Do You Actually Need?

Before you even think about filling out an application, you need to get crystal clear on what your kitchen actually needs to run. It's so easy to get carried away with a long wish list, but a strong lease application starts with a plan that’s both realistic and easy to justify.

Start by sorting your list into two columns: "must-haves" and "nice-to-haves."

A pizzeria, for example, absolutely has to have a high-capacity pizza oven and a walk-in cooler. Those are non-negotiable. That fancy, high-tech dough sheeter, though? That might be a "nice-to-have" that can wait for a later day. This kind of focused thinking shows leasing companies that you've got a solid, practical business plan.

Bundling Smaller Items into a Lease Package

It’s a common myth that leasing only makes sense for those huge, five-figure pieces of equipment. But what about all the smaller essentials? The blenders, food processors, prep tables, and shelving that every kitchen needs? Paying for all of that with cash can drain your startup fund in a hurry. This is where bundling comes in. Many financing partners allow you to group multiple smaller items into a single lease package, as long as the total value meets their minimum requirement, which is often around $1,000. This strategy is a game-changer, letting you get everything you need to be fully operational from day one without wiping out your cash reserves.

Think about it this way: instead of buying a commercial deep fryer outright and then trying to scrape together cash for the rest of your fry station, you can bundle it all together. You could lease the deep fryer, the dump station, the breading station, and even the initial set of fry baskets under one simple agreement. This turns a dozen small, cash-draining purchases into one predictable monthly payment. It’s a smart way to manage your budget and get a complete, professional setup while keeping your working capital free for things like inventory and marketing. To see how this could work for your kitchen, you can explore different restaurant equipment financing options.

Step 2: Get Your Financial Paperwork in Order

Leasing companies are, at the end of the day, financial partners. They need to see that your business is a solid bet. To prove that, you'll need to pull together a financial package that tells a clear story about your restaurant's health and its potential for success. Getting organized here is the key to a fast, painless approval.

Here’s a typical checklist of what you'll need:

- Business Plan: A detailed look at your concept, who you're selling to, and your financial projections.

- Recent Bank Statements: Lenders usually want to see 3-6 months to verify your cash flow.

- Tax Returns: Plan on having both your personal and business returns from the last 1-2 years ready.

- Credit Score Report: It's smart to know your score beforehand. Most lessors are looking for a score of 620 or higher.

Having all these documents ready to go before you even make the first call shows you're professional and will seriously speed up the whole process.

Step 3: How to Find the Right Leasing Company

With your equipment needs defined and your paperwork in order, it’s time to find the right partner. Not all lessors are created equal. You’re looking for a company that knows the foodservice industry, offers transparent terms, and has great customer support. Don't just jump at the first offer you get.

When you're exploring different financing options, reaching out to a firm's capital division, like the kwilladvisors' Capital division, can be a smart move. They often have specialized knowledge that can help you find the right financial product for your situation.

The right leasing partner is more than just a lender; they are a strategic ally who is invested in your restaurant's success. Take your time, ask plenty of questions, and compare multiple offers before you commit to anything.

Step 4: Nail Your Lease Application

Your application is your official pitch to the leasing company. Any missing info or little inconsistencies can cause big delays or even get you denied. Double-check every single detail before you hit that "submit" button, and make sure the equipment quotes you're providing are final and from the supplier you've chosen.

This is where all your prep work pays off. A clean, well-organized application backed by strong financials and a clear business plan makes the underwriter's job easier and builds a powerful case for your approval. You can learn more about how to lease restaurant equipment without losing your lunch money in our detailed guide.

Step 5: Read the Fine Print (Seriously)

Once you get that approval, you’ll receive the final lease agreement. This is, without a doubt, the most critical step in the entire process. Read every single line of that contract before you sign anything, and pay close attention to the fine print. This document will define your entire relationship with the lessor for years to come.

Zero in on these key areas:

- Monthly Payment Amount and Term Length: Make sure they match what you discussed.

- End-of-Lease Options: Understand exactly what your choices are—can you buy it, renew the lease, or do you have to return it?

- Hidden Fees: Keep an eye out for any administration, documentation, or late payment fees.

- Insurance and Maintenance: Get clarity on who is responsible for insuring the equipment and who pays for repairs.

The demand for these agreements is only growing. The commercial cooking equipment market was valued at $13.7 billion in 2023 and is projected to hit $18.6 billion by 2034, all driven by the constant need for new gear in a booming restaurant industry. Taking the time to master this process will ensure you get the tools you need to succeed.

Common Leasing Mistakes and How to Avoid Them

Navigating a commercial kitchen equipment leasing agreement can feel a little tricky, but sidestepping a few common mistakes can make a world of difference. Honestly, knowing what not to do is just as important as knowing the right steps to take. If you approach the lease process with a critical eye, you can protect your business from surprise costs and future headaches.

Think of it this way: you wouldn't sign a rental agreement for your restaurant space without reading every single clause, right? Your equipment lease deserves that same level of attention. Rushing through it can lock you into unfavorable terms that put a strain on your finances for years.

Overlooking the Details in Your Contract

This is hands-down the most common—and most expensive—mistake I see business owners make. It’s easy to spot the big terms like the monthly payment and the length of the lease, but the real devil is in the details buried in the contract language. These clauses spell out your responsibilities and all the potential extra costs.

I remember a caterer who signed a lease for several holding cabinets, thinking the return process at the end would be no big deal. Tucked away in the fine print was a clause making them responsible for all crating and freight costs to a specific return depot hundreds of miles away. That little oversight turned into an unexpected bill for over $2,000.

A lease agreement is a legally binding contract. Just assuming you understand it without reading every single line is a huge financial risk. The time you spend reviewing the document now is a direct investment in your business's financial health.

To avoid this, carve out some uninterrupted time to read the entire document. No exceptions. If any term is fuzzy or unclear, ask for clarification in writing before you even think about signing.

Miscalculating the True Cost of Your Lease

That monthly payment figure is only one piece of the financial puzzle. So many first-time lessees get blindsided when the total cost of leasing ends up being higher than they calculated. This happens when they forget to account for the other fees and obligations that pile up over the life of the lease.

Always factor in these extra expenses before you commit:

- Insurance Costs: Most leasing companies will require you to carry insurance on the equipment, and they’ll want to be named as the loss payee. This is an extra monthly or annual expense you absolutely must budget for.

- Maintenance and Repairs: Unless it’s spelled out differently in the contract, you're on the hook for all the upkeep. A single service call on a commercial refrigerator can easily set you back hundreds of dollars.

- Taxes: You will almost certainly be responsible for paying property taxes on the equipment you're leasing.

- Late Fees and Penalties: Make sure you understand the financial hit you’ll take for a late payment. These penalties can be steep.

By adding up these potential costs from the get-go, you get a true, honest picture of your financial commitment. This ensures your commercial kitchen equipment leasing plan is genuinely affordable and won't lead to nasty surprises.

Ignoring Your End-of-Lease Options

So, what happens when your lease is up? The answer should be crystal clear from day one. Many business owners get so focused on the immediate need for the equipment that they completely forget to plan for the end of the term. This leads to confusion and, you guessed it, more costly surprises.

Your options will depend entirely on the type of lease you signed. A $1 buyout lease is simple—you pay a buck and the equipment is yours. But with a Fair Market Value (FMV) lease, you might have to negotiate a purchase price, return the equipment (and pay for shipping!), or renew the lease. Not knowing these details ahead of time puts you in a weak negotiating position when the term expires.

Before you sign anything, make sure you can answer these questions:

- What are my exact obligations if I decide to return the equipment?

- How is "fair market value" actually calculated if I want to buy it?

- What are the terms and costs if I want to renew the lease instead?

Getting clarity on these points gives you a solid exit strategy that aligns with your long-term business goals. It turns your lease from a potential hidden liability into a strategic asset.

Leasing vs. Buying: Which Is Right for Your Kitchen?

You've seen the perks, you know the different types of leases, and you're aware of the common pitfalls. Now comes the moment of truth. The choice between commercial kitchen equipment leasing and buying isn’t about finding a one-size-fits-all "better" option. It’s about making a strategic call for your specific business, right now.

Think of it like choosing between a sprinter and a marathon runner. Leasing is your sprinter—built for speed, agility, and the flexibility to pivot on a dime. Buying is the marathon runner, designed for the long haul with a focus on endurance and the ultimate prize of ownership. To pick your champion, you need to take a good, hard look at your finances, your business model, and where you want to be in a few years.

The Best Times to Lease Your Equipment

Leasing absolutely shines in certain situations, especially when holding onto your cash and staying nimble are your top priorities. If your business falls into one of these buckets, leasing is probably the smartest financial play.

- Startups and New Concepts: When you're just starting out, cash is everything. Leasing lets you launch with a top-notch, fully equipped kitchen without burning through your precious startup capital on assets that immediately start to lose value.

- Tech-Dependent Kitchens: Does your menu lean heavily on the latest combi ovens, sous-vide machines, or advanced POS systems? Leasing gives you a massive advantage. You can upgrade every few years, ensuring you always have the best tools without getting stuck with outdated tech.

- Businesses Exploring New Ventures: Thinking of adding a food truck to your catering company? Leasing lets you outfit that new venture with almost no financial risk. If the concept doesn't take off, you aren’t left trying to sell off thousands of dollars in specialized equipment.

When Buying Your Equipment is the Smarter Choice

On the other hand, for established businesses with solid cash flow and a clear vision for the future, buying your equipment outright is a powerful move.

Purchasing is often the way to go when:

- You Have Strong Capital Reserves: If you can handle the upfront cost without choking your day-to-day cash flow, buying eliminates those monthly lease payments and starts building equity in your assets.

- The Equipment Has a Long Lifespan: Those foundational workhorses—like stainless steel prep tables, sinks, and classic gas ranges—have an incredibly long, useful life. It makes a ton of sense to buy these items since they won't become obsolete anytime soon.

- You Want Total Control: When you own it, it’s yours. You can modify it, move it, or sell it whenever you want, no need to get permission from a leasing company.

This decision becomes especially critical during a major undertaking, like remodeling an office space into a restaurant, where it shapes your entire financial blueprint from day one.

Your final decision should be a calculated one, based on a simple question: Will this choice give my business more financial power and operational freedom, both today and three years from now?

In the end, whether you lease or buy, the goal is the same: building a successful and profitable kitchen. By weighing these scenarios against your own situation, you can confidently choose the strategy that paves the smoothest road to success.

Taking Advantage of Tax Deductions

Beyond preserving cash, leasing offers a powerful financial perk that can directly impact your bottom line: tax deductions. In many cases, your monthly lease payments can be treated as an operational business expense, similar to rent or payroll. This means you can often deduct the full payment from your taxable income, which can lower your overall tax bill at the end of the year. This structure also simplifies your financial planning. As we covered in our guide to leasing, lease payments are usually fixed, giving you predictable monthly costs that make budgeting and forecasting much more accurate. It’s a straightforward way to manage expenses while gaining a valuable tax advantage.

Considering Long-Term Value and Obsolescence

The restaurant industry moves fast, and so does its technology. Buying a piece of equipment means you own it, for better or for worse—even when a newer, more efficient model comes out next year. This is where leasing, especially an operating lease, becomes a strategic tool for keeping your kitchen modern. It allows you to easily upgrade your equipment as technology improves, so you’re never weighed down by aging assets. This is especially true for tech-heavy items like POS systems or combi ovens. Leasing gives you access to the latest and greatest tools, ensuring your kitchen stays competitive without the long-term financial commitment of ownership.

Beyond Leasing and Buying: Other Equipment Options

While leasing and buying are the two main highways for outfitting your kitchen, they aren't the only routes to your destination. For savvy restaurant owners, especially those working with a tight budget, a little creativity can unlock some powerful alternatives. These options can help you get the high-quality tools you need without taking on the long-term commitment of a lease or the massive upfront cost of a purchase. It’s all about finding the right financial tool for the job and stretching every dollar as far as it can go. Thinking outside the box can be the very thing that protects your cash flow and sets your new venture up for success from day one.

Exploring these strategies isn't about cutting corners; it's about being resourceful. From finding incredible deals on perfectly functional equipment with minor cosmetic blemishes to securing funding designed specifically for small businesses, there are plenty of ways to build the kitchen of your dreams. Some of these paths offer direct savings, while others provide the capital you need to make smart purchases. Let's look at a few of the most effective alternatives that can help you get your doors open and start serving customers without breaking the bank.

Finding Deals on "Scratch and Dent" Equipment

One of the smartest ways to save a significant amount of money is to explore the world of "scratch and dent" equipment. These are brand-new, top-quality items that have minor cosmetic imperfections—like a small dent on a side panel or a scratch on a door—that happened during shipping or in the warehouse. These flaws have absolutely no impact on the machine's performance, but they result in a huge discount. You can often find this equipment through special outlet sales or auctions, allowing you to get a premium commercial refrigerator or deep fryer for a fraction of its retail price. It’s a fantastic strategy for acquiring the workhorse pieces for your kitchen while keeping more of your capital free for other essentials.

Exploring Microloans and Small Business Grants

If you need a capital injection to purchase equipment, don't overlook funding sources designed to support entrepreneurs. Microloans, often provided by non-profits or community development financial institutions, offer smaller amounts of capital with more flexible lending criteria than traditional banks. They are perfect for financing a few key pieces of equipment. On the other hand, small business grants are essentially free money—non-repayable funds awarded to businesses that meet specific criteria. The U.S. Small Business Administration (SBA) is an excellent resource to discover local and federal programs that can provide the cash you need to buy your equipment outright, completely debt-free.

Considering Merchant Cash Advances as a Last Resort

A Merchant Cash Advance (MCA) is another way to get cash quickly, but it should be approached with serious caution. With an MCA, a company gives you a lump sum of cash in exchange for a percentage of your future credit and debit card sales. While it’s fast and doesn't require a strong credit history, it is an extremely expensive form of financing with high fees that can quickly eat into your profit margins. Before even considering an MCA, you should exhaust every other possibility, including traditional loans and dedicated restaurant equipment financing programs, which offer much more favorable and predictable terms. Think of an MCA as an emergency option, not a primary funding strategy.

Got Questions About Equipment Leasing? We've Got Answers.

Even after getting the hang of how leasing works, you probably still have a few specific questions bouncing around. That’s completely normal. This is where we tackle the common "what ifs" and "how does this work" queries we hear from restaurant owners all the time.

Think of this as a final walkthrough to clear up any confusion so you can move forward feeling confident about your kitchen's next big step.

What Credit Score Do I Need to Lease Kitchen Equipment?

This is easily one of the most common questions, and while every leasing company has its own standards, a personal credit score of 620 or higher is a great starting point. For lenders, this number is often a quick signal of financial reliability, especially for a new spot that doesn't have years of business history to show off yet.

Now, if you're running an established restaurant with solid, consistent revenue, you'll likely find that lenders are a bit more flexible. They'll also look at how long you've been in business and your overall cash flow. If your credit is a bit rocky, don't sweat it just yet. Some companies specialize in financing for owners with lower scores, though you might see slightly higher rates.

Your credit score is a big piece of the puzzle, but it's not the whole thing. A well-thought-out business plan and healthy bank statements can make a huge difference, often strengthening your application even if your score isn't perfect.

Options for Business Owners with Bad Credit

If your credit score is lower than you’d like, don’t immediately count yourself out. A less-than-perfect credit history is not a deal-breaker in the world of equipment financing. Many online lenders and financing companies specialize in working with business owners who have faced financial hurdles. They understand that a credit score is just one part of your story. These lenders often place more weight on other factors, like the consistency of your cash flow and how long you've been in business. While you might face higher interest rates, the door to getting the restaurant equipment you need is still very much open.

How to Strengthen a Weaker Application

If you know your application has some weak spots, you can take proactive steps to make it more appealing to lenders. Start by getting all your financial documents in order, including recent bank statements and tax returns, to paint a clear picture of your business's health. It also helps to offer a larger down payment, which reduces the lender's risk and shows you have skin in the game. You could also bring in a co-signer with strong credit to back your application. Taking these steps can significantly improve your chances of approval and help you secure better terms.

A Word of Caution on "No Credit Check" Lenders

You’ll likely come across lenders promising "no credit check financing" or "guaranteed approval." While this can sound like the perfect solution, you should approach these offers with extreme caution. Often, these are red flags for predatory lenders who charge incredibly high interest rates and hidden fees that can trap your business in a cycle of debt. Reputable financing partners will always perform some kind of review to assess risk. It’s far better to work on strengthening your application for a legitimate lender than to get locked into an unfavorable agreement that could hurt your business in the long run.

Can I Lease Used Kitchen Equipment?

You absolutely can, and it can be a brilliant move. Many leasing companies are perfectly happy to finance used and refurbished kitchen equipment. Going for pre-owned gear is a fantastic strategy for slashing your monthly payments while still getting the high-quality, durable equipment your kitchen needs. It's an incredibly popular route for startups and anyone keeping a close eye on their budget.

Just a heads-up: before you sign on the dotted line, you'll want to be sure about the condition of the equipment and see if there are any warranties still in play. The leasing company will also want to approve the vendor you’re buying from and might even require a professional inspection. It's just their way of making sure the used items are a sound investment for everyone involved.

What Happens When My Kitchen Equipment Lease Is Over?

What happens at the end of your term really comes down to the type of lease you signed from the get-go. It's super important to understand these endgame options before you sign, as they shape your total costs and what you can do with the equipment long-term.

Here’s a quick rundown of the usual paths:

- Operating Lease: This is the simple one. When the term is up, you typically just return the equipment to the leasing company. Easy peasy.

- Capital Lease: This route gives you choices. You can often purchase the equipment for a price you agreed on upfront (sometimes for as little as a $1 buyout), renew the lease for another term at a lower rate, or return it.

Is Maintenance Included in My Lease?

This is a point of confusion for a lot of folks, and the short answer is: probably not. While some high-end, full-service leases will bundle maintenance and repair costs into your monthly payment, that's definitely not the standard arrangement.

More often than not, keeping the equipment in good working order—all the upkeep, maintenance, and repairs—falls on you, the lessee. Always, always clarify this in your lease agreement. If maintenance is your responsibility, remember to factor those potential service costs into your budget to avoid any nasty financial surprises down the road.

Ready to explore flexible and affordable equipment solutions for your kitchen? The experts at The Restaurant Warehouse can help you find the perfect leasing program to fit your budget and business goals. Learn more at https://therestaurantwarehouse.com.

Key Takeaways

- Protect your startup capital by leasing major equipment: Leasing converts a huge upfront purchase into a predictable monthly expense, keeping your cash free for crucial needs like payroll, marketing, and inventory.

- Match the lease type to the equipment's lifespan: Use a Capital Lease (rent-to-own) for long-term workhorses like ovens and walk-in coolers, and an Operating Lease (long-term rental) for tech that changes quickly, like POS systems, so you can easily upgrade.

- Look beyond the monthly payment to find the true cost: Your total financial commitment includes insurance, maintenance, taxes, and potential end-of-lease fees, so read the entire contract to understand these obligations and avoid expensive surprises.

Related Articles

About The Author

Sean Kearney

Sean Kearney is the Founder of The Restaurant Warehouse, with 15 years of experience in the restaurant equipment industry and more than 30 years in ecommerce, beginning with Amazon.com. As an equipment distributor and supplier, Sean helps restaurant owners make confident purchasing decisions through clear pricing, practical guidance, and a more transparent online buying experience.

Connect with Sean on LinkedIn, Instagram, YouTube, or Facebook.