A Guide to Leasing Commercial Kitchen Equipment

Leasing commercial kitchen equipment can be a seriously smart financial play, especially when you're trying to outfit a kitchen without dropping a massive amount of cash all at once. It's a strategy that gives you predictable monthly payments and the freedom to upgrade to newer, more energy-efficient gear down the line, keeping your cash flow healthy for all the other things a restaurant needs to thrive.

The Strategic Edge of Leasing Kitchen Equipment

In the fast-paced restaurant world, being quick on your feet financially is just as important as having a killer menu. This is where leasing your kitchen equipment becomes less of a simple transaction and more of a game-changing strategy. It’s not just about dodging a huge purchase price; it’s a calculated move that helps your restaurant stay nimble and competitive.

This approach is a lifesaver for new restaurants or anyone looking to expand. Instead of sinking thousands of dollars into a top-of-the-line combi oven or a massive walk-in freezer, you can put that capital to work elsewhere.

Preserve Capital for Growth

By leasing, you're freeing up cash for the things that actually drive business forward. Think about it:

- Marketing campaigns to get new faces in the door.

- Hiring and training an amazing front-of-house and back-of-house team.

- Investing in quality inventory for that ambitious new seasonal menu.

This kind of financial flexibility is huge. It lets you ride the unpredictable waves of the restaurant business without being weighed down by assets that are losing value every single day.

Stay Competitive with Modern Technology

The culinary world never sits still, and neither does the technology that powers it. Leasing gives you access to the latest and greatest equipment without the forever-commitment of buying it.

When a more efficient fryer or a smarter POS system comes out, leasing makes it way easier to upgrade. This keeps your kitchen running at peak performance and helps you stay one step ahead of the competition. For a deeper dive, you can explore the benefits of restaurant equipment financing in our detailed guide.

The reality is that leasing shifts risk. Instead of being stuck with outdated equipment, you transfer the risk of obsolescence to the leasing company, allowing you to adapt to changing trends.

The impact of this strategy is huge. In North America, the foodservice equipment leasing market was valued at over USD 25.8 billion. This just goes to show how essential leasing is for staying agile, especially with independent restaurants making up 40% of that market. You can discover more insights about this trend and its impact on the foodservice sector on GrandViewResearch.com.

So, What Equipment Does Your Kitchen Actually Need?

Jumping into a lease agreement without a crystal-clear idea of your kitchen's needs is like trying to cook a five-course meal without a recipe. It just doesn't work. Before you even think about signing on the dotted line, you have to do a serious audit of your menu, your workflow, and the physical space you're working with.

This isn't just busywork—it's the foundational step that prevents you from overspending and ensures every single piece of equipment has a job to do.

Start by breaking down your menu, item by item. What are your signature dishes? What specific cooking processes do they require? A ghost kitchen running a burger concept and a salad bar will have wildly different needs than a small café focused on espresso and pastries. Your menu is the blueprint for your entire equipment list.

This process naturally helps you separate the "must-haves" from the "nice-to-haves." That six-burner range and convection oven? They're probably non-negotiable workhorses. But does that specialty sous-vide machine truly earn its keep, or is it just going to take up valuable counter space?

Moving From Menu To Machine

Once you have a list of required processes, you can start translating them into specific appliances. Don't just jot down "fryer"; get specific about the capacity needed to handle your busiest Friday night rush. This is where you connect your culinary vision to the nitty-gritty of operational reality.

For each potential piece of equipment, you need to consider a few critical factors:

- Space and Layout: Will that new walk-in cooler actually fit through the door? Measure everything twice. Seriously.

- Power and Utilities: Does your building have the correct voltage and gas hookups for what you need? An unexpected electrical upgrade can absolutely destroy your budget.

- Energy Efficiency: A more energy-efficient appliance might have a slightly higher monthly lease payment, but it can save you hundreds on utility bills over the course of a year.

This strategic approach helps you build a smart, efficient kitchen from the ground up. For a great starting point, our detailed restaurant kitchen equipment checklist can guide you through organizing your selections.

The Financial and Strategic Impact

Defining your needs is also a major financial move. The global market for commercial kitchen equipment rentals was valued at around USD 1.8 billion in 2023 and is expected to nearly double by 2032. This growth is being driven by smart businesses, especially small and medium-sized ones, that use leasing to avoid huge upfront costs and put their capital to better use.

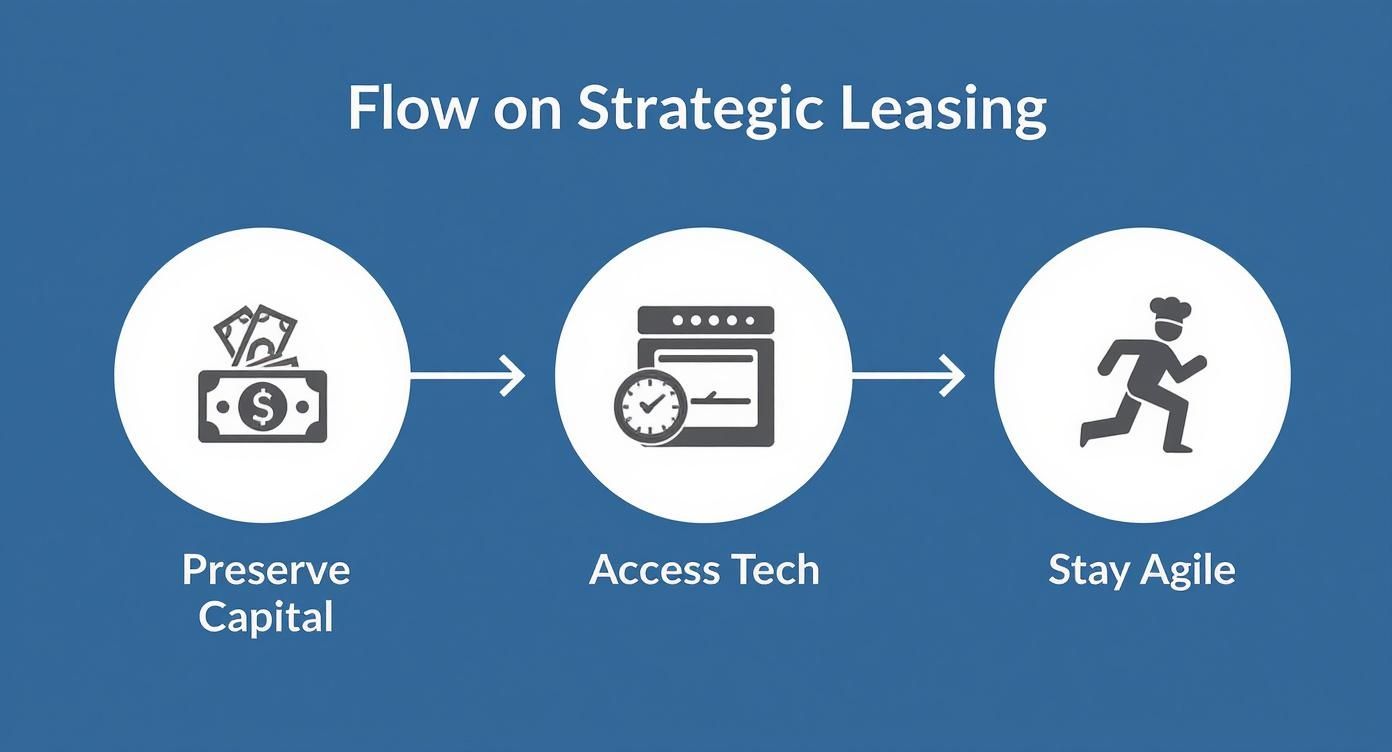

This infographic shows how a thoughtful approach to leasing can help preserve capital, give you access to modern tech, and keep your business agile.

As you can see, leasing isn't just about saving money today; it's about building a flexible and resilient business for tomorrow.

A well-defined equipment list is your best negotiation tool. It shows leasing companies that you are a serious, organized operator who understands their business inside and out, which can lead to better terms and a more favorable agreement.

Deciding whether to lease or buy can be tough, especially for big-ticket items. This table breaks down the decision-making process for some common pieces of kitchen equipment to help you weigh the pros and cons for your specific situation.

Lease vs Buy Analysis for Common Kitchen Equipment

| Equipment Type | Best for Leasing If... | Best for Buying If... | Typical Monthly Lease Cost |

|---|---|---|---|

| Commercial Refrigerator | ...you're a startup preserving cash or need flexibility to upgrade as you grow. | ...it's a core, long-term workhorse and you want to build equity in your assets. | $75 - $200 |

| Six-Burner Range | ...you want to test a new menu concept without a huge capital outlay. | ...it's central to your daily operations and you plan to use it for 5+ years. | $100 - $250 |

| High-Capacity Fryer | ...your menu's focus on fried items might change or you want to try a specialty model. | ...fried food is your signature, and you need a heavy-duty unit built to last. | $80 - $180 |

| Commercial Dishwasher | ...you prefer predictable monthly payments that include service and maintenance. | ...you have the capital and want the lowest total cost of ownership over a decade. | $150 - $400 |

Ultimately, this analysis should be guided by your business plan and financial projections. What makes sense for a pop-up might not work for an established restaurant group.

Your goal is to create a list that supports your business without any unnecessary bloat. As you finalize your choices, it’s also a great idea to explore articles discussing innovative kitchen products. This ensures you’re aware of the latest options that could boost efficiency or open up new menu possibilities. This thoughtful planning is what sets the stage for a successful and profitable kitchen operation.

Decoding the True Cost of Your Equipment Lease

That low monthly payment you see advertised? Think of it as just the tip of the iceberg. To really get a handle on what leasing commercial kitchen equipment will cost you, you’ve got to dig into the fine print and uncover the expenses hiding below the surface. If you don't, you could be setting yourself up for some nasty budget surprises down the road.

A good lease is one with no financial shocks. That means doing your homework and accounting for every possible cost from the day you sign until the day the term ends.

Uncovering the Hidden Costs

The monthly payment is your starting point, but it's rarely the final number. A handful of other fees and obligations are almost always part of the deal, and they can add a pretty significant chunk to your total expenses. Getting ahead of them is your best defense against unexpected bills.

Here are the usual suspects you need to budget for:

- Down Payments: Even though leasing helps you hold onto your capital, many agreements still need some money upfront—often the first and last month's payment.

- Insurance Obligations: You’ll be on the hook for insuring the equipment. The leasing company needs to protect its asset, and that cost is passed on to you.

- Maintenance and Repair Fees: Get crystal clear on who fixes what. Some leases might bundle in a service package, but many leave you fully responsible for upkeep and repairs.

- Delivery and Installation: Don’t just assume shipping and setup are included. These costs can easily tack on hundreds of dollars to your initial outlay.

You absolutely have to get these details in writing. If a leasing agent gives you a vague answer about who handles maintenance, that should be a massive red flag.

Planning for the End of the Lease

So, what happens when the lease is up? This is a question you need to answer from day one, because your decision will have real financial consequences. Your options depend entirely on your specific agreement, but they almost always involve a final cost.

Your end-of-lease choices will likely include one of these:

- Returning the Equipment: Sounds simple, right? But you could be hit with fees for de-installation, shipping, and any wear and tear they deem "excessive."

- Renewing the Lease: You can often extend the agreement, sometimes at a lower rate, but you’re still making monthly payments.

- Purchasing the Equipment: Leases with a $1 Buyout option make this cheap. But with a Fair Market Value (FMV) lease, you’ll have to pay whatever the equipment is worth at that moment—which could be thousands of dollars.

Understanding your end-of-lease options is not a future problem—it's a current budgeting requirement. The potential cost of a buyout or return fees should be factored into your financial forecasts today.

Let's say a small bakery is leasing a high-end convection oven on a three-year FMV lease. If that oven’s fair market value is projected to be $2,500 at the end of the term, they should be setting aside about $70 a month to prepare for the buyout. This simple bit of foresight turns a potential financial shock into a manageable, planned expense, making the whole process of leasing commercial kitchen equipment much smoother.

Finding the Right Lease Type and Partner

Okay, you’ve figured out exactly what equipment your kitchen needs. Now comes the part that can feel just as crucial: picking the right lease agreement and, just as important, the right company to work with.

It's a common misconception that all leases are the same. They’re not. The partner you choose and the type of lease you sign can have a huge impact on your restaurant's financial health and how much flexibility you have down the road. This decision is all about matching the lease structure to your long-term plans. Do you see yourself owning this equipment in a few years, or would you rather upgrade to the latest tech when your term is up?

Comparing Common Lease Structures

You'll quickly run into two main types of leases: the Fair Market Value (FMV) lease and the $1 Buyout lease. They're built for very different goals and have completely different financial setups.

-

Fair Market Value (FMV) Lease: Think of this as a true rental. You'll get lower monthly payments, which is great for cash flow. When the lease term ends, you can choose to buy the equipment for whatever it’s worth at that time, return it, or simply renew the lease. This is a fantastic option for tech-heavy equipment that might be outdated in a few years, or if keeping your monthly costs super low is your top priority.

-

$1 Buyout Lease: This one operates a lot more like a traditional loan. The monthly payments are higher, but at the end of the term, you can buy the equipment for a symbolic price—usually just a single dollar. This is the smart path for foundational, built-to-last equipment you know you’ll be using for many years.

The choice between an FMV and a $1 Buyout lease really boils down to one question: Is this equipment a temporary tool or a long-term asset? Answering that honestly will keep you from getting stuck in a deal that doesn't fit your business.

How to Vet a Potential Leasing Partner

The company you lease from isn't just a bank; they're a partner. A great one gets the pressures of the restaurant industry. A bad one? They can become a massive headache that disrupts your entire operation.

Before you even think about signing a contract, do your homework on any potential partner. A bit of due diligence right now can save you a world of stress later. For a deeper dive, our guide on obtaining restaurant equipment through a lease agreement has some great insights.

Here’s a quick checklist to run through when you're evaluating companies:

- Industry Reputation: Do they actually specialize in the restaurant business? Look for online reviews and testimonials from other owners, and give their Better Business Bureau rating a look.

- Customer Service: Just call them. Can you easily get a human on the phone? If they're hard to reach during the sales process, imagine what it'll be like when you have an urgent problem.

- Contract Transparency: Ask for a sample agreement. A trustworthy partner will provide clear, easy-to-understand terms without burying things in jargon or hidden clauses. Pay close attention to the details on maintenance responsibilities and your end-of-lease options.

- Flexibility: Does the company offer options to buy out early or upgrade your equipment mid-lease? Your business is going to evolve, and you need a lease that can adapt with you.

The industry is changing fast, especially with the growth of concepts like ghost kitchens and food trucks. This has pushed the commercial kitchen equipment rental market to offer more flexible options. You're seeing more companies offer subscription-based models with simple, predictable monthly costs—a fantastic choice for smaller businesses. Choosing a partner who offers these modern, flexible solutions is a good sign they know where the industry is headed.

Time to Talk Terms: How to Negotiate Your Lease Agreement

Here's a little secret a lot of restaurant owners miss: that lease agreement the agent slides across the table isn't set in stone. Many people treat it like a take-it-or-leave-it deal, but the reality is that most terms are more flexible than you think. A bit of confident, well-prepared negotiation can literally save you thousands over the life of the lease.

Think about it—you're the customer here. Any good leasing company wants to build a long-term relationship, not just make a quick buck. They're often willing to bend a bit to win your business. So, never be afraid to ask for what you want. The worst they can say is no.

Know What You're Fighting For

Before you even think about picking up the phone, you need to know your non-negotiables. Sure, a lower monthly payment is what everyone wants, but there are other, more strategic points in a contract where you can score a huge win for your business. Focus your energy on the terms that will have the biggest impact on your cash flow and day-to-day operations down the road.

Make these points the focus of your conversation:

- The Interest Rate (or "Money Factor"): This is where the leasing company makes its profit. If you’ve got a solid credit history and a strong business plan, you have some serious leverage to ask for a better rate. Don't be shy.

- Term Length: Are you looking for lower monthly payments or a lower total cost? A shorter term means higher payments but you'll pay less interest overall. A longer term drops your monthly outlay but costs more in the long run. Negotiate a term that lines up perfectly with your financial forecasts.

- The Buyout Clause: Get clarity on your end-of-lease options from day one. If it’s a Fair Market Value (FMV) lease, can you get a more favorable buyout price or a cap written into the contract from the start?

- Maintenance and Repair Clauses: This is a big one. Who pays when that shiny new oven breaks down? Push for the leasing company to cover major repairs, or at the very least, negotiate a clear cap on your out-of-pocket maintenance costs.

Don't get tunnel vision on the monthly payment. A slightly higher payment in exchange for a killer maintenance package and a favorable buyout option is often a much smarter financial move for the long haul.

Putting It Into Practice: A Real-World Scenario

Let's say you're negotiating a lease for a combi oven. The agent comes back with an offer for a 36-month lease with a 12% interest rate and an FMV buyout.

Instead of just accepting, you could counter with something like this:

"Thanks for the proposal. Our business is in a strong financial position, and we've already secured favorable rates on other financing. I'd be ready to sign today if we could bring that interest rate closer to 8.5%. Also, to make my end-of-term budgeting more predictable, I'd like to cap the FMV buyout at $1,500."

This approach is powerful because it’s specific, professional, and you've given a logical reason for your request. You've shown them you’ve done your homework and you're a serious operator, which instantly gives you more credibility.

Red Flags to Watch Out For in the Fine Print

A good negotiation isn't just about what you can get—it's also about what you avoid. Be extremely wary of any agreement loaded with harsh penalties or vague, fuzzy language. These are often signs that you're dealing with an inflexible or potentially predatory leasing partner.

Keep an eye out for these contractual landmines:

- Excessive Early Termination Penalties: Life happens. If you need to end the lease early for some reason, the penalty should be reasonable. A clause requiring you to pay the entire remaining balance plus extra fees is a massive red flag.

- Vague Maintenance Terms: Phrases like "lessee is responsible for all routine maintenance" are way too broad. What's "routine"? Demand a specific, itemized list of what is and is not covered.

- Automatic Renewal Clauses: Watch out for sneaky clauses that automatically roll you into a brand new lease term if you don't provide written notice months in advance. You should always have control over the renewal process.

Successfully negotiating your agreement for leasing commercial kitchen equipment comes down to protecting your business. A fair, transparent contract is the foundation for a healthy partnership and, ultimately, a thriving kitchen.

Common Questions on Leasing Kitchen Equipment

When you're looking into leasing kitchen equipment, a lot of questions are bound to pop up. It’s a big decision, and getting clear, straightforward answers is the key to feeling confident you're making the right move for your business. Let's tackle some of the most common things operators ask.

What Happens If Leased Equipment Breaks Down

This is probably the most critical question on anyone's mind, and the answer comes down to the fine print in your lease agreement. It's something you absolutely need to clarify before signing.

Many lease structures, especially Fair Market Value (FMV) leases, roll maintenance and repairs right into the deal. If your oven suddenly quits during a dinner rush, you just make a call to the leasing company. They handle everything—sending a technician, ordering parts, or even swapping it out.

On the other hand, a $1 Buyout lease often puts all the maintenance responsibility squarely on your shoulders. Before you commit, ask them point-blank: "What's the exact process for reporting a problem?" and "What's your guaranteed response time?" A good leasing partner will have a crystal-clear service plan ready to go.

Can I Upgrade My Equipment During the Lease Term

Yes, and this is one of the biggest advantages of leasing. The ability to upgrade is a huge win for keeping your kitchen efficient and up-to-date.

Most leasing companies have flexible upgrade options built right in. This lets you trade an older model for a newer, better one, often with just a small tweak to your monthly payment. This is especially valuable for tech-heavy equipment like combi ovens or POS systems that are constantly evolving. Make sure you talk about the upgrade process from the get-go so you know about any costs and how it affects your current terms.

Think of leasing as a subscription to the best tools for your kitchen. When a better, faster, or more energy-efficient model comes out, you have a clear path to get it without being stuck with outdated assets.

What Credit Score Is Needed for an Equipment Lease

There isn't a single magic number here, as every leasing company has slightly different standards. As a general rule, a personal credit score of 650 or higher is a great starting point and will usually get you the best terms and lowest rates.

But don't panic if your score isn't perfect. Many lenders who specialize in the foodservice industry look at the bigger picture. They'll consider other factors, like:

- How long you've been in business

- Your monthly revenue and cash flow

- A solid, well-thought-out business plan

If you're a startup or have a lower credit score, you can still get approved, but you might be looking at a higher interest rate or be asked for a larger security deposit.

And while you're focused on the financial side, don't forget about your kitchen's infrastructure. Down the line, you might need reliable commercial plumbing services to keep up with the demands of a high-volume kitchen.

Is It Better to Lease from a Manufacturer or a Third Party

Both approaches have their own distinct perks, and the best choice really depends on your situation.

Leasing directly from a manufacturer means you're getting deep product expertise. They know their equipment inside and out and sometimes offer promotional financing deals that are tough to beat.

A third-party leasing company, however, offers incredible variety. They let you bundle equipment from completely different brands—say, a Vulcan range, a Hobart mixer, and a True refrigerator—all under one simple lease. Third-party financers also tend to have a wider network of lending partners, which can spark more competition and lead to better rates for you. The right call depends on whether you're loyal to a single brand or want to mix and match the best tools for each job.

At The Restaurant Warehouse, we provide flexible leasing and financing options designed specifically for the foodservice industry. Equip your kitchen with top-tier brands without the upfront capital strain. Explore our financing solutions and get your kitchen running today.

About The Author

Sean Kearney

Sean Kearney is the Founder of The Restaurant Warehouse, with 15 years of experience in the restaurant equipment industry and more than 30 years in ecommerce, beginning with Amazon.com. As an equipment distributor and supplier, Sean helps restaurant owners make confident purchasing decisions through clear pricing, practical guidance, and a more transparent online buying experience.

Connect with Sean on LinkedIn, Instagram, YouTube, or Facebook.